Enterprise Strata Insights

Analysis, strategy and operational intelligence for enterprise strata management professionals

The Non-Event Close: Why Year-End Should Be a Review, Not a Rebuild

For many strata firms the financial year-end is a multi-week scramble: an audit assembled from scratch, an annual activity report pulled from disparate systems, an AGM pack built by hand. For a few it is a non-event. The difference is not effort or headcount, but whether the year's operational activity and notice-of-AGM content were recorded as they happened, ready for low-touch or zero-touch compilation and distribution.

Read

Two Roads to the Agent: Why StrataPort Is Building MCP and Native APIs in Parallel

Anthropic is wiring everything to a structured protocol called MCP. OpenAI is teaching Codex to drive the same screens humans drive. The strata platforms that survive the next two years will refuse to pick a side.

Read

From Chatbot to Colleague: What Agentic AI Actually Means for Strata Operations

80% of Australian strata businesses are now using AI tools, but 24% are deploying AI agents, autonomous systems that execute multi-step workflows. That 24% marks the beginning of a structural shift.

Read

The Compliance Reset: What the April 2026 NSW Strata Reforms Mean for Every Manager in Australia

The most operationally significant NSW strata reforms since 2015 took effect on 1 April. They standardise the data at scheme inception, and that changes everything for technology platforms.

Read

The 2026 Benchmarking Verdict: What 1.4 Million Lots Reveal About Where Strata is Heading

The Macquarie Bank 2026 Strata Benchmarking Report is the industry's most comprehensive dataset. Here's what it confirms, what it challenges, and what it means for platform strategy.

Read

The Onboarding Trap: Why the First 48 Hours Define the Next 12 Months

Every levy notice, every payment reference, every welcome pack inherits whatever data quality was established at go-live. When onboarding is treated as an admin task instead of a risk management function, the costs compound.

Read

The Integration Imperative: Why Your Strata Platform's Connectivity Matters More Than Its Feature List

The strata platforms that win in 2026 aren't the ones with the longest feature list, they're the ones that connect intelligently to banks, suppliers, government registries, and owner services.

Read

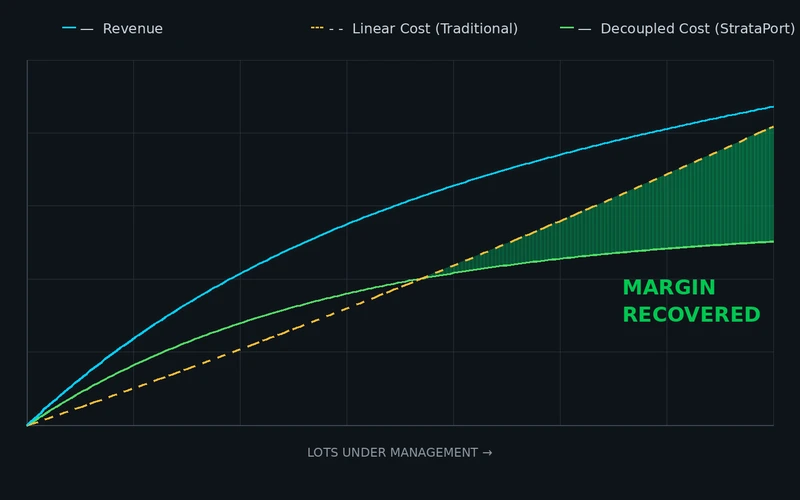

The Efficiency Ceiling: Why Linear Headcount Growth is Failing Enterprise Strata

Macquarie Bank data released last month shows mid-tier strata firms losing margin despite fee increases. Automation-driven decoupling is the only path to profitable scale.

Read

The Trust Accounting Automation Playbook: Why Daily Balancing is Just the Starting Line

For most enterprise firms, daily bank reconciliation is now standard practice. But balancing the books doesn't mean you've optimised the workflow. This article explores the next level of trust accounting automation.

Read

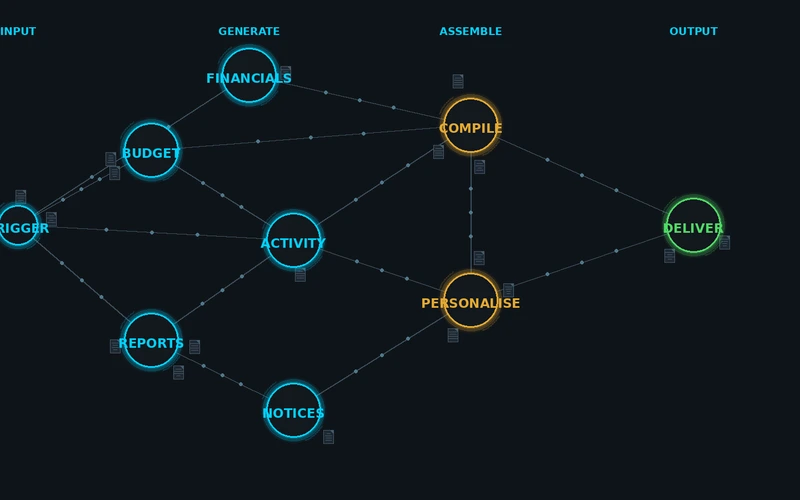

Anatomy of Zero-Touch AGM Setup: What Replaces Pressing the Button

A step-by-step breakdown of how StrataPort's AGM automation generates, compiles and distributes dozens of documents without human intervention.

Read

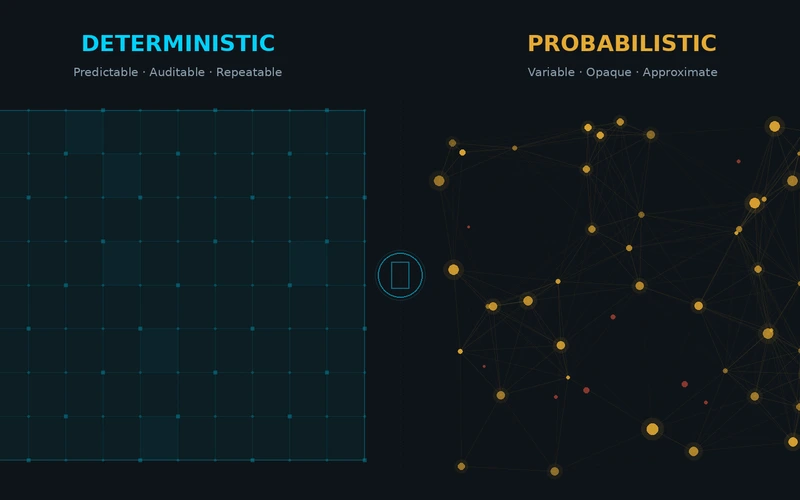

Deterministic vs Probabilistic: Why We Don't Put AI in the Automation Pipeline

The case for rules-based automation in trust accounting and compliance, and where AI actually belongs in the strata management stack.

Read

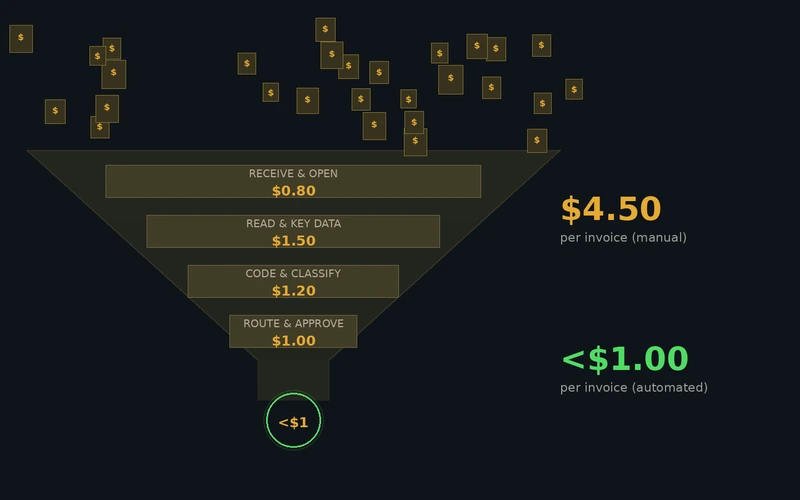

The Supplier Invoice Black Hole: Quantifying the Hidden Cost of Manual Processing

When you process 50,000 invoices a year at $4.50 each in labour, the numbers are staggering. Here's the unit economics case for API-driven automation.

Read

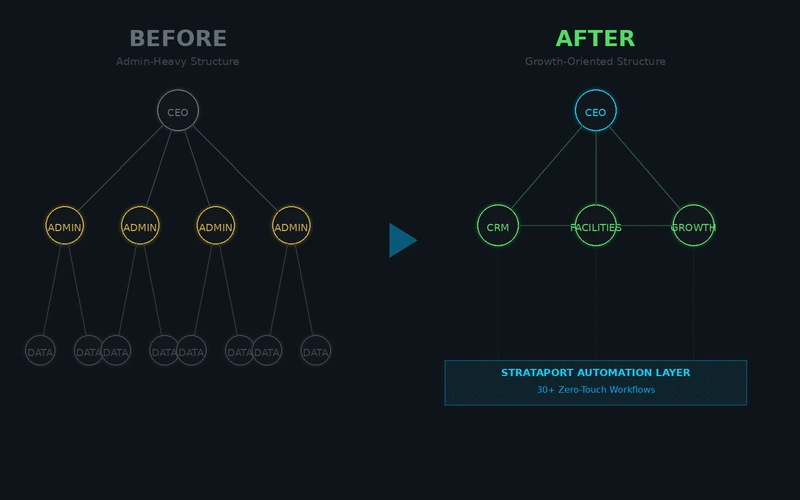

From Admin Manager to Growth Leader: Redefining the Strata Executive Role

Automation isn't about replacing staff, it's about funding the client relationship and technical facilities roles that justify premium fees and prevent churn.

Read